Why Critical Illness Coverage Is Smarter Than Ever—A Reality Check

I used to think critical illness insurance was just another monthly bill—until I saw how fast hospital bills piled up for a friend. That wake-up call made me dig deeper. Today’s healthcare costs are unpredictable, and having the right protection isn’t just wise—it’s essential. This isn’t about fear; it’s about being prepared. A diagnosis like cancer, heart attack, or stroke doesn’t just bring physical pain—it brings financial strain that can last years. Medical treatments are more advanced now, but they come at a cost. Even with health insurance, families often face thousands in out-of-pocket expenses. Add in time off work, travel for specialized care, and long-term rehabilitation, and the numbers grow fast. This article explores why critical illness coverage has evolved into a smarter, more strategic part of financial planning than ever before—and how it protects not just your health, but your life’s stability.

The Hidden Cost of Getting Sick

When someone is diagnosed with a serious illness, the focus is rightly on healing. But behind the scenes, a parallel crisis often unfolds—one measured in dollars and cents. The true cost of a critical illness extends far beyond hospital bills and prescription drugs. It includes income lost during recovery, transportation to treatment centers, home modifications for accessibility, childcare arrangements, and even nutritional supplements not covered by standard health plans. These expenses are rarely discussed, yet they can accumulate rapidly. For example, a single round of specialized cancer therapy may cost tens of thousands, even after insurance covers its portion. Deductibles, co-pays, and non-covered services add up. A patient might need to travel weekly to a regional medical center, incurring fuel, lodging, and meal costs over months. These are real burdens that savings accounts were never designed to handle.

Consider a woman in her early 50s diagnosed with early-stage breast cancer. Her health insurance covers surgery and chemotherapy, but she must pay 20% of certain diagnostic imaging costs, which alone amount to $4,000. She takes three months off work, losing $15,000 in income. She rents a temporary apartment near the treatment facility for six weeks, spending another $3,500. Her husband reduces his hours to help with care, cutting household earnings further. Without disability insurance, these losses go uncompensated. In less than a year, the family faces over $30,000 in direct and indirect costs. This scenario is not extreme—it’s increasingly common. According to studies, nearly half of Americans would struggle to cover a $1,000 medical emergency. When the figure jumps into the tens of thousands, the strain becomes overwhelming. Relying solely on emergency funds is risky, especially when retirement savings or college funds are diverted to cover illness-related costs.

The emotional toll is matched by financial instability. Families may delay major life decisions—selling a home, retiring, or supporting children’s education—because resources are redirected to survival. Some turn to credit cards or personal loans, trapping them in cycles of debt. Others reduce contributions to retirement accounts, weakening long-term security. The ripple effect touches every corner of financial life. This is where critical illness insurance plays a unique role. Unlike traditional health insurance, which pays providers directly, critical illness policies deliver a tax-free lump sum directly to the policyholder upon diagnosis of a covered condition. That money can be used freely—to cover medical co-pays, replace lost income, pay for transportation, or simply keep the household running. It’s not a cure, but it’s a buffer that preserves dignity and choice during one of life’s most vulnerable periods.

How Critical Illness Coverage Actually Works

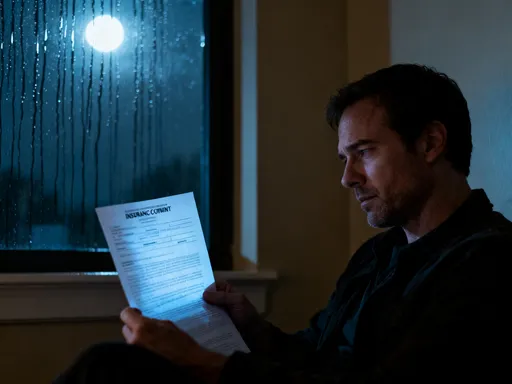

Critical illness insurance remains one of the most misunderstood financial tools. Many confuse it with health insurance or disability coverage, but it serves a distinct purpose. At its core, it is a supplemental plan that provides a one-time cash payment if the insured is diagnosed with a qualifying serious condition. These typically include heart attack, stroke, major organ transplant, end-stage renal failure, and various forms of cancer. The list varies by insurer, but most policies cover between 30 and 50 specific illnesses. Once a diagnosis is confirmed and the claim is approved, the insurer issues a lump sum—often within weeks. There are no restrictions on how the money is spent. This flexibility is central to its value. Whether it goes toward medical bills, mortgage payments, or hiring a caregiver, the decision rests entirely with the individual.

It’s important to clarify what critical illness insurance does not do. It does not pay doctors or hospitals directly. It does not replace comprehensive health insurance. Instead, it fills gaps that health plans leave open—particularly those related to income loss and non-medical expenses. For instance, while health insurance might cover the cost of a coronary bypass, it won’t compensate for the six weeks the patient cannot work. Disability insurance could help, but it often has waiting periods and requires ongoing proof of inability to work. Critical illness coverage, by contrast, pays out quickly after diagnosis, providing immediate liquidity. This speed can make a tangible difference, especially in the early, chaotic days following a diagnosis when decisions must be made fast.

The application process typically involves a health questionnaire and sometimes a medical exam. Insurers assess risk based on age, family history, lifestyle, and pre-existing conditions. Premiums are generally fixed for the term of the policy and can be paid monthly or annually. Policies may be offered through employers or purchased individually. One key feature is that benefits are paid only once per illness, though some plans allow partial payouts for less severe stages of disease, such as early-stage cancer. Additionally, some modern policies offer living benefits, meaning they can pay a portion of the benefit if the insured needs long-term care or suffers a second critical illness after a waiting period. These enhancements reflect how the product has evolved to meet changing healthcare realities.

Why Now Is the Right Time to Reassess Your Protection

The relevance of critical illness coverage has grown significantly in recent years, driven by broader economic and healthcare trends. Medical costs continue to rise faster than inflation, with hospital stays and advanced treatments becoming increasingly expensive. At the same time, people are living longer, which means more time spent managing chronic conditions and higher odds of facing a serious diagnosis. Recovery periods have also lengthened. Treatments that once required weeks of recuperation now often demand months of follow-up care, monitoring, and therapy. All of this extends the financial exposure far beyond the initial hospital stay.

Another major shift is in the world of work. More people are employed in freelance, contract, or gig economy roles, where employer-sponsored health and disability benefits are limited or nonexistent. Even in traditional jobs, benefit packages have become leaner, with higher deductibles and narrower coverage. As a result, individuals bear more financial responsibility than ever before. A 2023 report found that nearly 40% of workers do not have access to disability insurance through their employer. Without it, a sudden illness can lead to rapid income loss. Critical illness insurance steps into this gap, offering a form of self-protection that aligns with today’s decentralized work landscape.

Demographics also play a role. The average age of first-time cancer diagnosis has shifted younger in some categories, and heart disease remains a leading cause of death across age groups. Women, who often serve as primary caregivers, face unique risks—not only to their own health but to their financial stability when caring for others. With life expectancy rising, the window for potential health crises has widened. Planning ahead is no longer optional; it’s a necessity. Insurers have responded by making policies more accessible, with streamlined underwriting, broader condition lists, and options for partial payouts. Some even integrate digital health tools to encourage preventive care. These changes make now an ideal time to evaluate whether you have adequate protection in place.

Spotting the Gaps in Your Current Plan

Many people believe they are financially protected because they have health insurance. While essential, health coverage alone is insufficient. It pays providers, not individuals. It covers treatment, but not lost wages, travel, or home care. A common misconception is that disability insurance fills all income gaps. Yet disability policies often have strict eligibility criteria and may not pay out unless the individual is completely unable to perform any job—not just their own. There are also waiting periods, sometimes lasting 90 days or more, before benefits begin. During that time, bills still come due. Critical illness insurance bridges these gaps by providing fast, flexible funds at the moment they are needed most.

To identify weaknesses in current protection, consider asking a few key questions. Does your health plan have a high deductible? Do you have savings that could cover three to six months of living expenses if you couldn’t work? Are you responsible for caregiving duties that would require paid help if you became ill? Is your job secure enough to allow extended unpaid leave? If the answers raise concerns, there may be exposure. Another red flag is assuming employer-provided benefits are permanent. Job changes, layoffs, or retirement can eliminate access to group plans. Individual policies, by contrast, stay with you regardless of employment status.

Real-life cases illustrate how small oversights lead to big consequences. A man in his 40s had group critical illness coverage through work but didn’t realize it was not portable. When he changed jobs, he lost coverage and didn’t replace it. Two years later, he suffered a stroke. Though he recovered physically, the financial damage was lasting—he had to dip into retirement savings to cover rehab and lost income. In another case, a woman assumed her policy covered all cancers. However, her plan excluded early-stage diagnoses, which is common in some older policies. When she was treated for stage one breast cancer, she received no payout. These examples underscore the importance of reading policy details carefully and updating coverage as life circumstances change.

Balancing Risk and Reward: The Financial Logic

Like any financial decision, critical illness insurance requires weighing costs against potential benefits. Premiums vary based on age, health, coverage amount, and policy features. For a healthy 45-year-old, a $50,000 benefit might cost between $40 and $70 per month. While that may seem significant over time, it pales in comparison to the potential cost of an untreated financial crisis. Consider it not as an expense, but as a transfer of risk. Just as homeowners insurance protects against fire, critical illness coverage protects against the financial fallout of disease. The likelihood of filing a claim is real: studies suggest that a 35-year-old has a 1 in 3 chance of making a critical illness claim before age 65. For women, the odds are slightly higher due to conditions like breast cancer and stroke.

The principle of risk pooling underlies all insurance. By paying a small, predictable premium, individuals join a larger group where only a fraction will experience a claim. Those who do are supported by the collective contributions. This system works best when people enroll early, while they are healthy. Waiting until symptoms appear or a diagnosis is near often means higher premiums—or denial of coverage altogether. Locking in a policy in midlife can secure favorable rates for decades. Some policies also offer return-of-premium options, where payments are refunded if no claim is made by a certain age, adding long-term value.

It’s fair to acknowledge that not everyone needs this coverage. Someone with substantial emergency savings, strong employer benefits, and multiple income streams may already have sufficient protection. But for many—especially single-income households, self-employed individuals, or those with limited sick leave—the added layer of security is invaluable. The goal is not to eliminate all risk, which is impossible, but to manage it wisely. Critical illness insurance doesn’t promise to prevent illness, but it does help ensure that a health crisis doesn’t become a financial collapse.

Practical Steps to Build Smarter Protection

Taking action starts with education and assessment. Begin by reviewing your current insurance landscape. List what you have—health, life, disability, any existing critical illness coverage—and note the benefit amounts, exclusions, and conditions. Look for overlaps and gaps. For example, does your disability policy cover partial disability? Does your health plan include out-of-network treatment costs? Once you understand your baseline, determine how much additional protection you might need. A common rule of thumb is to aim for a benefit that covers 6 to 12 months of essential expenses, including mortgage, utilities, groceries, and transportation.

Next, compare policies from multiple insurers. Pay close attention to the list of covered conditions, waiting periods, and exclusions. Some policies exclude pre-existing conditions or impose limitations based on lifestyle factors like smoking. Others offer riders for children or spouses, allowing family-wide protection. Consider whether you want a level premium policy, where rates stay the same, or an annually renewable one, which may start cheaper but increase over time. Working with an independent financial advisor or insurance broker can provide objective guidance, especially since they are not tied to a single company and can present a range of options.

Timing matters. Applying while you are healthy increases your chances of approval and better rates. Delaying until you have a health scare may close the door entirely. If you’re between jobs or transitioning careers, securing individual coverage ensures continuity. Finally, integrate this protection into your broader financial plan. Treat it like any other essential expense—part of a holistic strategy that includes budgeting, saving, and investing. Regularly revisit your policy, especially after major life events like marriage, childbirth, or buying a home. Protection is not a one-time decision, but an ongoing commitment to resilience.

Beyond the Payout: What You’re Really Protecting

In the end, critical illness coverage is about more than money. It’s about peace of mind. It’s the knowledge that if the unthinkable happens, your family won’t face impossible choices—between treatment and rent, or between recovery and financial survival. It preserves autonomy. Instead of rushing back to work before healing is complete, a person can focus on getting better. Instead of draining retirement savings, a family can maintain their long-term goals. The emotional relief is profound. Stress weakens the immune system and slows recovery. Financial security, by contrast, creates space for healing, both physical and mental.

For caregivers—often spouses or adult children—the impact is equally significant. They can afford help without guilt. They can take time off without fear. The policy doesn’t just support the patient; it supports the entire ecosystem of care. In this way, critical illness insurance becomes a quiet guardian of family stability. It reflects a deep form of love—an investment in the people who matter most. It says, “I’ve thought ahead. I’ve done my part to protect us.”

This isn’t about anticipating disaster. It’s about respecting the fragility and value of everyday life. Modern medicine gives us more second chances than ever before. Critical illness coverage ensures that those second chances come with the financial breathing room needed to truly take them. It’s not a bet on sickness. It’s a vote of confidence in recovery, resilience, and the power of preparation. In a world of uncertainty, that confidence may be the most valuable protection of all.